Key Takeaways

- Corporate bank account applications have a lengthy and complicated process

- Banks have an extensive screening process to filter out any companies that are deemed risky

- There is a cycle of credit and applications that most founders get caught up in

- There are steps to take that will solidify a company and improve the likelihood of getting approval

In the case of many entrepreneurs looking to establish a presence in Japan, registering a company is surprisingly simple. However, opening a corporate bank account can prove to be a little less straightforward.

Many business owners assume the opening of a bank account automatically follows the process of legally incorporating their company. When in reality, Japanese banks very frequently reject corporate account applications—especially when they come from newly established foreign-owned companies. Rejections do not usually offer explanation, oftentimes leaving founders confused and delaying everything from invoicing and payroll to visa applications and business operations.

The good news is that these rejections often have a root cause. Japanese banks follow strict compliance procedures and evaluate every application through a risk-management lens. Understanding the bank’s acceptance process can dramatically improve your chances of approval.

Why is opening a corporate bank account in Japan so difficult for foreign entrepreneurs?

As a foreign founder, you might find unique challenges that do not apply to Japanese citizens. Rejection is often driven by risk management and regulatory compliance rather than discrimination or business quality.

Japanese banks are known for their very conservative means of operating. In order to combat fraud and financial crimes, Anti money laundering (AML) and Know Your Customer (KYC) requirements have become increasingly strict. This forces banks to dive deep when faced with new unknown companies. This becomes hard when foreigners apply for a bank account because of the limited visibility into overseas owners, international transactions, and cross-border corporate structures.

It is common for entrepreneurs to believe that this acceptance from the banks is based primarily on their nationality. When in reality, banks are primarily focused on reducing risk. Their goal is to ensure they understand everything about the company such as who owns the company, how it operates, where money comes from, and whether future transactions can be monitored effectively.

How do Japanese banks evaluate corporate bank account applications?

The Invisible Risk Scoring System

Most banks will never show applicants their internal review criteria, but applications are effectively evaluated using a series of risk-based questions:

- Can we verify this company actually exists?

- Can we identify the real owners?

- Does the business model make sense?

- Can we predict future transaction activity?

- Is there a money laundering or fraud risk?

- Is there a responsible contact person in Japan?

- Does this company appear likely to remain operational long-term?

This perspective helps explain why perfectly legal businesses can still be rejected. The issue is often not legality; it is uncertainty. Banks generally prefer businesses they can easily understand and monitor.

Business Legitimacy Matters More Than Most Founders Realize

Banks increasingly expect evidence that a company is already preparing to conduct real business.

Supporting materials that strengthen an application include:

- A detailed business plan

- Revenue projections

- Customer contracts or letters of intent

- Supplier agreements

- Marketing materials

- A functioning company website

Missing these elements may cause a bank to view the company as a shell entity rather than an operating business.

")

Why Do Japanese Banks Reject Corporate Bank Account Applications?

Understanding how banks assess applications can help founders proactively address potential concerns before applying.

The “Invisible Risk Scoring” system banks apply

This system is put into place to test whether they can understand, verify, and monitor the proposed business. It essentially tracks the perceived risk level that banks would be willing to accept. Companies that are deemed safe usually have clear and well defined answers to these questions:

- Can the company’s operations be verified?

- Are the beneficial owners clearly identifiable?

- Does the business model make commercial sense?

- Can transaction patterns be reasonably predicted?

- Are there elevated money laundering risks?

- Is there a responsible contact person in Japan?

- Does the company appear stable enough to operate long term?

This perspective offers an angle as to why perfectly legal businesses can still be rejected. The issue is often uncertainty, not legality. Banks tend to only trust businesses they can easily understand and monitor.

Beneficial ownership and corporate structure verification

Banks increasingly expect evidence that a company is already preparing to conduct real business. Ownership transparency influences approval. This transparency could be backed by offshore holding companies, venture capital investment structures, and nominee agreements. The easier it is for banks to understand ownership structures, the smoother the review process.

Corporate Bank Accounts

Get Your Corporate Bank Account Approved in Japan

- Documents structured for Japanese bank review from day one.

- Guidance on business plan, ownership structure, and local presence.

- Trusted by 100+ companies incorporated across Japan.

Why do Japanese banks reject corporate bank account applications?

Although banks rarely disclose specific reasons for rejection, several common factors consistently contribute to unsuccessful applications. One of the biggest challenges for foreign founders is demonstrating a meaningful connection to Japan.

Lack of ties to Japan

Many banks strongly prefer having a representative who resides in Japan and can be contacted easily if questions arise. While not always legally required, local representation significantly improves credibility.

Weak business credibility or insufficient operating history

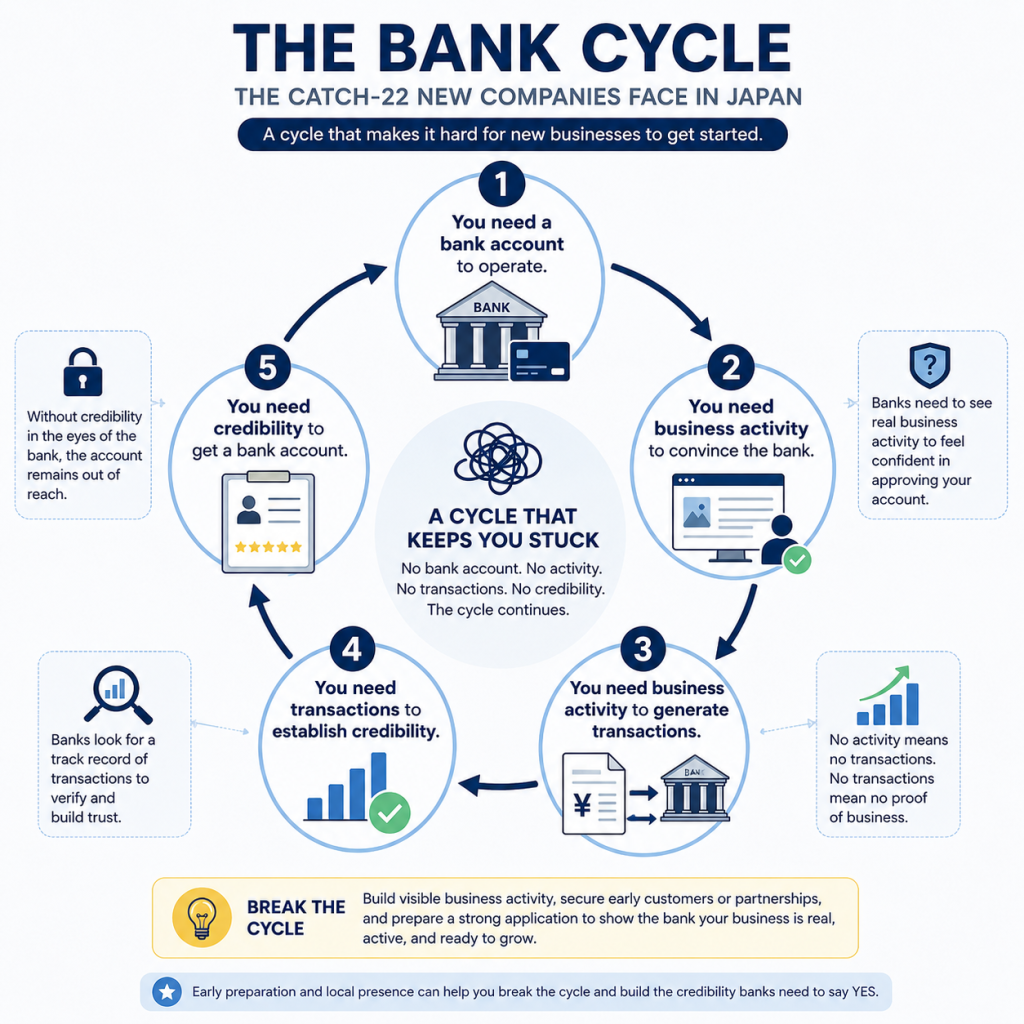

New companies tend to face a credibility gap. Founders often submit applications before securing customers, partnerships, or contracts. Unfortunately, this can create a perception that the business is not yet operational. This complicates the situation, as a history is important to secure a contract or deal, but these histories are built on these contracts. Banks may become concerned when they see no customers, business activity, website, etc. This is particularly common among early-stage startups and foreign founders entering Japan for the first time. This creates a cycle that many founders fall into.

Virtual office arrangements and limited physical presence

Many startup founders choose virtual offices to reduce costs. However, banks often view virtual offices with caution because they make it more difficult to verify business operations. That said, a virtual office is not necessarily a dealbreaker. Companies may still be approved if they can demonstrate local management, clear business activities, and existing customers.

Language and communication barriers

Another barrier that could pop up is a communication barrier. Most banking interactions are conducted strictly in Japanese. This is normally a struggle because most of the time new foreign founders have little to no Japanese fluency. This proposes the issue of not being able to clarify any complex points. There is also limited access to English-speaking banking staff

High-Risk Business Models

Certain industries consistently receive additional scrutiny because they involve complex transaction flows or heightened compliance risks.

| Business Type | Why Banks May Be Concerned |

| Cryptocurrency/Web3 | AML and regulatory concerns |

| Import/Export | Complex international transactions |

| Consulting | Difficult-to-verify revenue |

| Affiliate Marketing | Limited transparency |

| Dropshipping | Cross-border payment flows |

| Overseas Recruiting | International money movement |

| AI & SaaS Startups | Intangible products and subscription revenue |

Why foreign founders often struggle with the “No Japanese Track Record” problem

How Japanese banks build trust

One of the most misunderstood aspects of Japanese banking is that overseas success does not automatically transfer into Japan. A founder could have a successful business overseas, significant revenue, etc. But banks often evaluate the company almost completely. Trust is frequently built through Japanese customers, business partners, suppliers, and phone numbers. This emphasis on local credibility reflects Japan’s broader business culture, which prioritizes stability, predictability, and long-term relationships.

How can foreign entrepreneurs improve their chances of approval?

Preparation before applying is often the biggest determinant of success. Once the first wall is broken, opportunities become easier and easier to obtain.

Establish a strong local presence

Establishing a local presence builds a foundation for proof that a company is legitimate and has ties to the local community. Some ways to do this include securing an appropriate office arrangement, obtaining a Japanese business phone number, and preparing Japanese-language materials.

Create a realistic and detailed business plan

Another way to build trust is through financial transparency. This includes explaining revenue generation clearly, providing achievable financial projections, and demonstrating understanding of the Japanese market. This transparency is often the major distinction between safe and unsafe companies to Japanese banking officials.

Prepare for enhanced compliance reviews

Compliance reviews also allow for Japanese banks to see into the operations of a startup company. Some ways to prepare for compliance reviews are to organize ownership documentation, anticipate and have an answer for AML related questions, and explain cross border transaction flows clearly.

Seek professional assistance when necessary

Help is almost always available, and a lot of times necessary. Some professional help might include help from people like administrative scriveners, tax accountants, and business consultants specializing in foreign companies.

Supporting evidence of business activity

Documentation check list:

- Revenue forecasts

- Client contracts or letters of intent

- Supplier agreements

- Invoices and purchase orders

- Clear and realistic business plans

- Revenue forecasts supported by evidence

- Japanese-language business materials

- Operational readiness

- Company registration certificate

- Articles of incorporation

- Identification documents for directors

- Proof of office address

Building a credible online presence

While having an established presence within Japan is important, an online presence is also necessary and goes hand in hand with setting a foundation for business. Simply having a website is not enough. Banks may review customer references, Japanese language content, and founder information.

What should you do if your application is rejected?

A rejection is not necessarily permanent. Many founders successfully obtain approval after strengthening their applications. There are multiple steps to take that could expose the holes in an operation, and then patch them up to make a fool proof plan.

Identify potential weaknesses in your application

The first step would be to find any weak spots in the application. This includes any missing documentation, limited business substance, lack of Japanese ties, and complex ownership structures.

Strengthen your business credibility before reapplying

The next step after finding the weak points of an application, is to strengthen them. Some ways to strengthen an application is to secure local clients, improve supporting materials, and enhance an online presence.

Consider alternative banking options

Another option would be to look at the situation from a whole new angle. It would be beneficial to weigh the options when it comes to who to utilize as a bank. Different banking systems offer different operating means and often have differing requirements. One banking option would be Megabanks. Megabanks often have extensive compliance requirements. They are large and established banks and because of that they often prefer established businesses. They are oftentimes more comprehensive with their documentation expectations.

The next option would be regional banks. These banks often have a relationship driven business approach. They tend to have a greater emphasis on local presence. They have potential advantages for regionally focused businesses, making it the most likely option for local businesses owners. The last option is digital banking. These often have faster onboarding processes and alternative verification methods, potentially making it more startup-friendly. Another option would be credit unions, which specialize in businesses with local community ties. For more information about specific banks, visit Guide to a Corporate Bank Account in Japan .

")

Corporate Bank Account Approval Readiness Checklist

Below is a tool to assess corporate bank account application readiness.

Readiness assessment

| Is a physical office secured? | YES/NO |

| Is a Japanese-language website launched? | YES/NO |

| Is a Business plan completed? | YES/NO |

| Is a Revenue model clearly documented? | YES/NO |

| Is a Japanese phone number available? | YES/NO |

| Are client contracts prepared? | YES/NO |

| Is ownership structure documented? | YES/NO |

| Are resident representatives available? | YES/NO |

Scoring Guide:

- 0–4 (YES) points: High rejection risk

- 5–7 (YES) points: Moderate rejection risk

- 8+ (YES) points: Strong application readiness

Frequently Asked Questions About Japanese Corporate Bank Account Rejections

Why do I keep getting rejected for a business bank account?

This is usually due to a lack of history, perceived riskiness, or lack of clarity.

Why is it so hard to open a bank account in Japan?

Banks have low acceptable levels of risk when it comes to businesses.

How do I open a corporate bank account in Japan?

Be sure that you check all of the boxes as to what banks check for in order to get approved.

Why was my business bank account application declined?

There were most likely flaws in the application process, such as not enough specifications or not enough ties to the Japanese Financial system.

Which Japanese bank is best for foreigners?

There are a few banks that are considered more accessible than others. Some examples of these banks are SMBC, Mizuho Financial Group, and MUFG. There are also other banks such as Resona Bank and Japan Post Bank. For more information on these banks, visit Guide to a Corporate Bank Account in Japan

Does visa status affect corporate bank account approval?

Yes, Visa status can affect corporate bank account approval. For instance, if the Visa held by the applicant is not a permanent resident Visa, then it is more likely to get declined. The application has a higher chance of getting accepted if the status of residence is three years or greater.

Can I open a corporate bank account using a virtual office?

Yes, it is possible to open a corporate bank account using a virtual office, but it is a lot harder. This is simply due to the fact that the lack of a physical location is seen as more risky to Japanese banks, and oftentimes this could be the reason why an application could be denied.